Have you ever found yourself dreaming of cruising down a scenic coastal highway in a sleek convertible, the wind whipping through your hair? I know I have. It’s precisely this desire for unique travel experiences that led me to discover Turo, the peer-to-peer car-sharing platform that’s revolutionizing the way we rent vehicles.

But as I delved deeper into the world of Turo, a nagging question kept popping up: Does my personal auto insurance cover a Turo rental?

This question isn’t just academic—it’s important for anyone considering using the platform.

After all, the last thing you want is to be caught in a sticky situation without proper coverage.

The Personal Insurance Landscape

When it comes to personal auto insurance, no two policies are exactly alike. It’s a bit like snowflakes—each one unique, with its own set of terms, conditions, and coverage limits.

But generally speaking, most personal auto insurance policies are designed with a specific set of circumstances in mind:

- Coverage for your own vehicle

- Protection while driving rental cars (in many cases)

- Liability coverage for accidents you might cause

But here’s the rub: Turo isn’t your typical rental car company. It’s a peer-to-peer platform, which means you’re renting from individuals rather than a corporation.

Personal Insurance and Turo: A Square Peg in a Round Hole?

I remember the first time I rented a car through Turo. The excitement of trying out a Tesla Model 3 was palpable. But as I reached for my keys, a thought struck me: “Wait, am I actually covered if something goes wrong?”

The truth is, most personal auto insurance policies weren’t written with peer-to-peer car sharing in mind. Here’s why this matters:

- Commercial Use Exclusion: Many personal policies exclude coverage for vehicles used for commercial purposes. Since Turo is a commercial platform, your policy might not apply.

- Rental Car Provisions: While your policy might cover traditional rental cars, Turo vehicles often fall into a gray area.

- Liability Limits: Even if your policy does provide some coverage, the limits might not be sufficient for a high-end Turo rental.

However, this is not exactly the situation with Geico. There have been compromise from GEICO over the past few years.

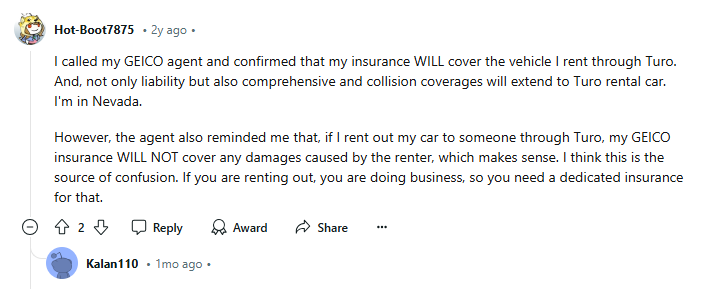

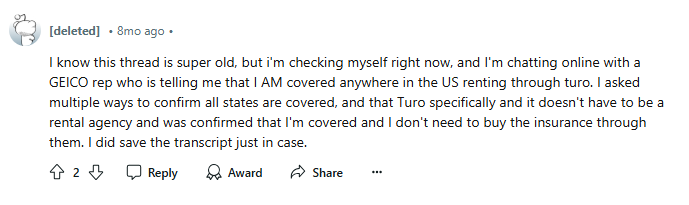

Does GEICO cover Turo?

From all indications, Geico’s coverage for Turo rentals varies significantly depending on the state and specific policy terms.

Some Geico representatives have confirmed coverage for Turo in certain states, including California, Washington, and Maryland.

However, other policyholders have reported being explicitly told that Geico does not cover Turo rentals, except in specific states like Alaska, Florida, Mississippi, North Carolina, New York, and West Virginia.

This variability underscores the importance of directly contacting Geico and obtaining written confirmation of coverage before renting through Turo.

- Coverage may depend on policy language regarding “personal vehicle sharing programs”

- Some policies explicitly exclude Turo rentals, while others treat them like traditional rentals.

- Policyholders are strongly advised to review their policy documents and consult with Geico representatives for clarity

- In cases where personal insurance doesn’t cover Turo rentals, considering Turo’s own protection plans may be prudent.

Geico may just be the least stringent insurance company with a policy around peer-to-peer car-sharing companies in comparison to companies like USAA, Progressive, and State Farm.

Turo’s Insurance Options: A Lifeline for Renters

Recognizing the insurance gap, Turo has developed its own insurance options.

These plans are designed to provide coverage specifically for peer-to-peer rentals. Here’s a quick rundown:

- Premier Plan: Offers the most comprehensive coverage

- Standard Plan: Provides a good balance of coverage and cost

- Minimum Plan: Offers basic protection for budget-conscious renters

Each plan comes with its own liability limits, deductibles, and additional features.

For instance, the Premier Plan includes primary coverage, which means you don’t have to involve your personal insurance at all in case of an incident.

But here’s something to keep in mind: Turo’s insurance isn’t free.

The cost is factored into your rental price, which means opting for more comprehensive coverage will increase the overall cost of your rental.

The Bottom Line

So, does personal insurance cover Turo rentals?

The answer, frustratingly, is: it depends. But armed with this knowledge, you’re now in a much better position to make informed decisions about your Turo adventures.

Here’s what I recommend:

- Review your personal auto insurance policy carefully. Look for any mentions of peer-to-peer rentals or car-sharing platforms.

- Contact your insurance provider directly. Ask them specifically about coverage for Turo rentals.

- Consider Turo’s insurance options. Weigh the costs against the potential risks of relying solely on your personal insurance.

- If you’re a frequent Turo user, explore specialized insurance products designed for the sharing economy.

The goal isn’t to discourage you from using Turo. On the contrary, I believe platforms like Turo offer incredible opportunities for unique travel experiences. The aim is to ensure you’re fully protected while enjoying these adventures.

As we wrap up this exploration, I’m reminded of a quote by the Roman philosopher Seneca: “Luck is what happens when preparation meets opportunity.” In the world of Turo and insurance, preparation means understanding your coverage options and making informed choices.

So, the next time you’re eyeing that dream car on Turo, take a moment to consider your insurance situation. A little forethought can go a long way in ensuring your journey is as smooth and worry-free as possible. After all, isn’t peace of mind the ultimate luxury in any travel experience?